How we approach credit risk scoring with Railz Credit Score

What is credit risk?

Credit risk is a broad term that refers to the risk of loss due to entities (people or businesses) failing to meet their financial obligations. In a functioning and vibrant economy there are borrowers and lenders, suppliers and buyers, investors and bond issuers, and credit risk is a necessary byproduct of economic activities. Inherent is the chance that borrowers do not repay lenders, or buyers do not pay suppliers. When this happens we say the debtor is in default, which can occur under an array of situations, such as lagging 90 or more days behind on payments, or filing for bankruptcy protection.

How is credit risk assessed?

Many years ago, credit risk was mainly assessed at the individual level through reputation and personal interviews. These methods are not scalable or objective, and lead to bias in credit offerings or scoring.

The credit risk assessment industry has grown significantly in recent years. In 2021, credit risk analysis is very sophisticated as the quantity of borrowers, along with the amount and availability of descriptive data has continually increased. Innovations in data science and the ability to benchmark profiles against a large set of data offer credit score providers and users new opportunities to assess risk. Ideally, this information can be accessed digitally through the client’s various accounts and financial and accounting service providers. However, for 69% of U.S. businesses, manual entry, such as through spreadsheets, still dominates much of the way financial information is maintained - which is error-ridden. Accessing accurate and real-time financial data on businesses is key for a creditor to assess risk and worthiness.

Who traditionally provides credit risk scoring?

Credit score providers exist for both retail customers, such as individuals, and large commercial customers. Retail credit reporting agencies such as TransUnion and Equifax report on the creditworthiness of individuals. While credit rating agencies such as Moody’s and S&P publish rankings of publicly-traded businesses on standardized scales.

Small- and medium-sized businesses (SMBs) sit somewhere in the middle, with characteristics of both retail and commercial borrowers. SMBs’ credit risk is often difficult to measure due to lack of credit history and survivorship bias. That is, SMBs with short or no credit history do not have enough information to make any reliable assumptions about future credit performance based on past performance; while those SMBs with longer credit history naturally have better credit performance, as those with poor performance will often cease operations. This can lead to challenges for the SMB market obtaining the credit they need for their business to succeed. At Railz, we have come up with solutions to provide better insights into SMBs using a holistic and historical look-back, plus real-time pull, of their financials. The Railz Credit Score is centred around finding a new way to judge the credit-worthiness of a business.

What is Railz Credit Score?

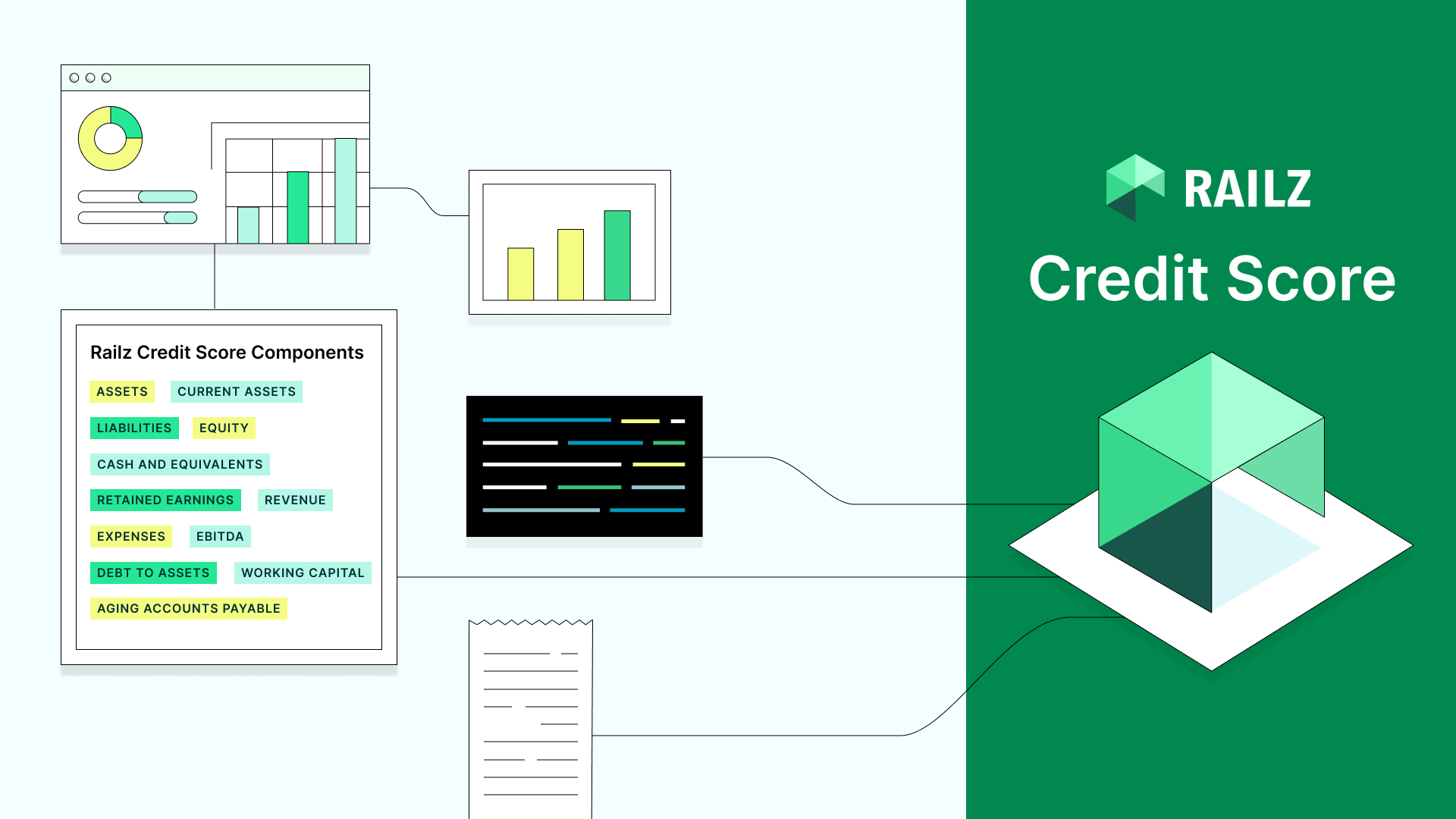

Data is plentiful, but leveraging this trove of information for credit risk purposes can be messy and difficult, as each data provider maintains their own individual data structures. Railz’s unique capabilities as an accounting and financial data normalization engine, present an exciting opportunity to provide analytics and insights into credit risk from accounting data. Railz uses structural credit models and machine learning to develop a holistic credit risk scoring system that is simple to use and understand. When a business registers with us through your financial service company, we provide a 36-month time series of probabilities of default, a proprietary score between 300 and 850, similar to a retail (FICO) credit score, and a mapping to an analogous Moody’s, S&P, DBRS, and Fitch score, and a digestible description of our assigned rating.

Railz’s analytics and insights suite takes a deep dive into the financials and behavioural patterns of borrowers, and our credit score can be considered an amalgamation of the available financial and accounting information a business can digitally provide. We are providing an alternative to an assessment of risk based on a single information source, such as past behaviour or balance sheet, as this may classify many new companies as unworthy of lending to, such as startups who do not own significant high-value assets. These companies, however, may have sufficient cash inflows to cover their obligations, or own intellectual property, which is difficult to value on the balance sheet but valuable to your institution as the lender or creditor. Each piece of information, while informative, can not provide the full picture of the health of a business alone. Factors that the Railz credit scoring algorithm incorporates include: balance sheet items such as assets and liabilities, income and cash flow statement items such as earnings and cash flow, financial ratios such as measurements of leverage and liquidity, and behavioural data. Railz handles this process every step of the way from the data normalization to the final credit score.

Why your financial institution should measure the credit risk of your SMBs in a new way

With modern analytics techniques, behaviours, risk indicators, and trends across a population can be applied at a low-level to gain insights on individual customers, which has uses in loan underwriting to assess the risk level of writing a loan, and deciding whether or not to take on that financial risk. Insights into a customer's individual risks also gives lenders flexibility to design products for unique or marginal borrowers, as opposed to simply approving or rejecting borrowers based on strict criteria and limited information. This provides your financial institution or financial technology company further opportunity to provide credit, funding, or lending opportunities to your target customer group.

Lending decisions for SMBs are often made on the basis of the business owner’s credit history or credit score via a credit reporting agency. While an important piece of information, relying on data related to the individual rather than the business means potentially rejecting low risk requests from strong companies. Consider the three C’s of credit: Character, Capital and Capacity. Character refers to the reliability of the borrower to repay debts, and is based on credit history. Capital refers to assets, including equipment, property or cash that could be liquidated in the event of a loss of income, the kind of information that can be found on a company’s balance sheet. Capacity refers to the borrower's ability to repay debt with their income, which can be found in the income statement.

Retail credit reporting agencies rely on “Character”-type information to determine credit scores based on prior performance from credit reports. Railz has developed a credit scoring system, specific to SMBs, that aims to fill in the gaps in Capital and Capacity considerations by putting accounting data to work. By leveraging accounting data we can provide credit insights on new businesses that don’t have a long credit history to pull from.

We’re excited to offer a credit score you can trust for your commercial customers

We know that high fidelity data and access to normalized financial data is key to the success of your financial institution - it’s why we built an API that empowers you to access all that information on your small- and medium-sized business customers. Our Credit Score is one way that we provide insights into your business customers that you could not have typically accessed from standard credit score providers. We look forward to seeing your institution provide funding to successful businesses and startups with our proprietary credit scoring capabilities.

Marie Osmun is a Senior Quantitative Developer at Railz. She joined Railz in July 2021 and brings with her more than five years of experience in financial consulting, developing quantitative credit risk and economic models. She spends her spare time baking cookies with her three year old daughter, maintaining a painting practice, and indoor gardening.